Emergency Fund Essentials: What Is Your Ideal Amount?

Are you prepared for financial disaster? An emergency fund can help you during an unexpected financial event or disaster.

Saving can be your personal safety net. An emergency fund can help to protect you when disaster strikes. Here is an emergency fund essential guide to help you discover your ideal amount to save.

What Is An Emergency Fund?

An emergency fund is a way to shield oneself when a problem arises. It provides a sense of financial security for when an issue happens that was not included in your annual budget. Some issues it could help to cover are unplanned:

Car repairs

Healthcare costs

Losing a job

Home repairs

Natural disasters

The money in an emergency fund is intended to help cover a portion or all of the costs.

Many Americans Lack An Emergency Fund

Bankrate reports that “more than half of Americans have less than three months’ worth of expenses in an emergency fund.” Many Americans have no rainy day fund to have enough to last three to five months. When the total percentage is calculated, seventy percent of Americans range from having no savings to only enough to last a few months.

Only twenty-five percent of those surveyed reported having enough savings to last six months or longer.

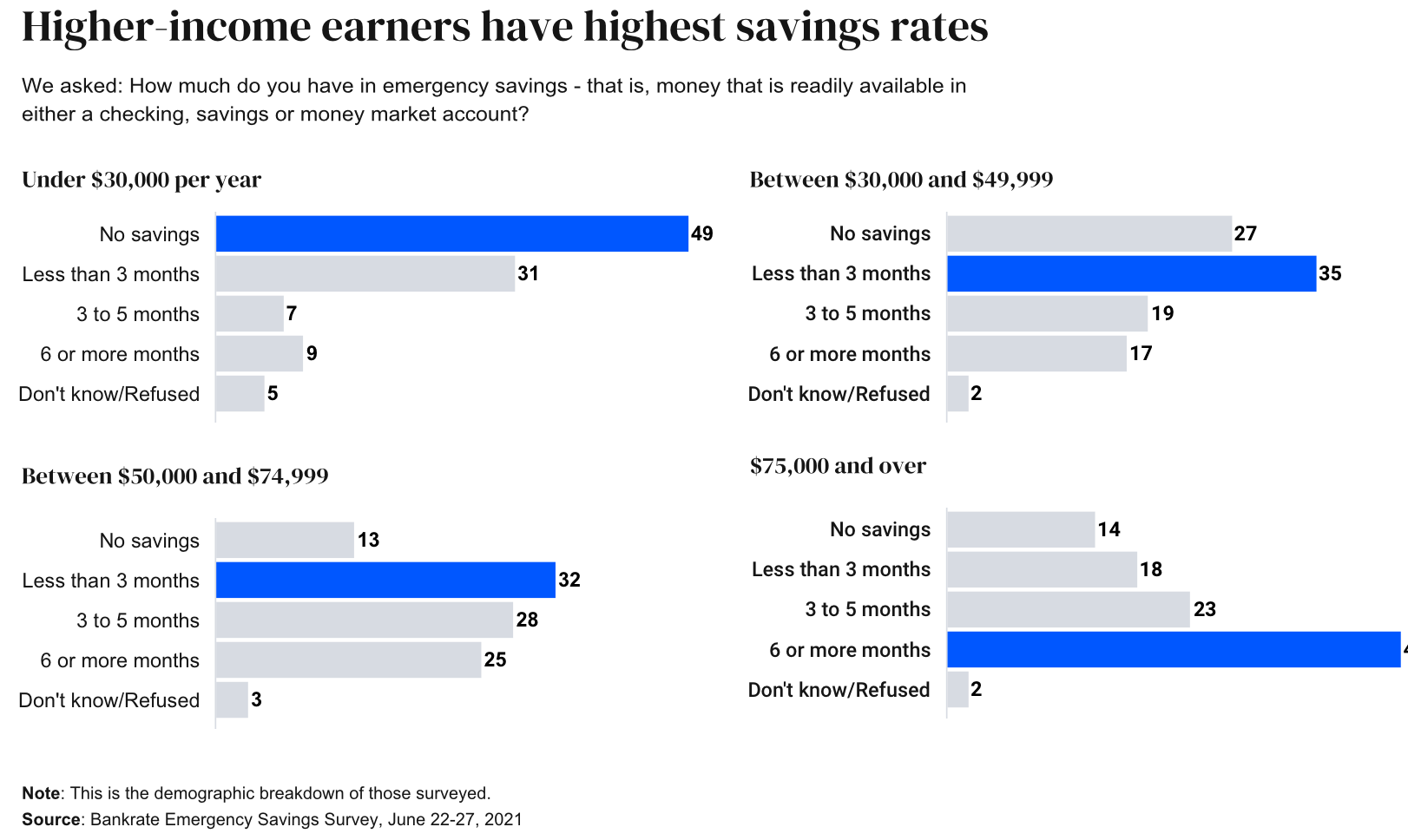

Bankrate broke it down further in the survey by comparing the income of people surveyed to the amount they had saved for a rainy day.

The above chart exemplifies that the more money a person makes, the more ability one can save if they do not live beyond their means.

How Much Money Should Be In My Emergency Fund?

The amount you need in an emergency fund will depend upon your financial circumstances, how much you want to put away, and the types of emergencies you want to prepare for.

General Rainy Day Fund

There could be a general emergency fund. A basic emergency fund could cover many emergencies to prevent you from dipping into your savings and retirement accounts.

To begin to build your financial cushion, know the monthly expenses of:

Rent or mortgage

Monthly grocery bill

Utility bill (water, garbage, recycling, gas, electric)

Telecommunication bill (Internet, phone, streaming services, cable)

Insurance payments (health, house, rent, car)

Monthly transportation costs (gas, car payment, public transportation)

Debt payments (credit card, student loans, car, medical, and any other loans)

A mortgage is a type of debt. Pay it off as soon as possible.

Any other expenses

Once you know how much is spent in those eight areas each month, calculate how much to save to have a six-month cushion in an emergency fund. Keep the emergency funds in a high-yield savings or money market account. Nerdwallet has an emergency fund calculator to simplify building a rainy day fund.

Other Emergencies To Plan For

Life happens. Life can get very expensive fast. An unplanned emergency or cost could arise even if you are financially stable. Here are three other emergencies to plan for that could happen to you.

Losing Your Job

You may have a job now. But it could be lost at any time. An economic recession or depression could happen that forces your employer to reduce its workforce to save the company money drastically.

Your boss or manager could fire you at any time for any reason. Someone willing to work for less could replace you. The company could work with contractors or freelancers instead of paying full-time employees.

As an employee, there is only the illusion of job security. Set aside enough money to last while you may have to look for another job if you get fired. It may be a good idea to consider starting a side hustle to bring in some extra income. You can then decide if you want to create your own business or not or continue to have a side project.

In the meantime, save money in case you lose your job.

Medical Emergencies Fund

Create an emergency fund for an unplanned healthcare emergency or surgery. Going to the emergency room or having surgery can be costly. With separate money set aside for a medical emergency, invest in a flexible spending account (FSA and a health savings account (HSA).

Debt dot org lists the average price of common surgeries in the United States:

Heart valve replacement: $170,000

Heart bypass: $123,000

Spinal fusion: $110,000

Hip replacement: $40,364

Knee replacement: $35,000

Angioplasty: $28,2000

Hip resurfacing: $28,000

Gastric bypass: $25,000

Cornea: $17,500

Gastric sleeve: $16,000

The cost of the surgery, along with the trip to the hospital and the hospital stay, can cost more than a person’s yearly salary. There is also the cost of recovery time. You may be out of work for a few months or longer, depending on your job type.

Education Fund

An education fund is included in this list. Some people go into debt for a college education. Many parents decide to go into debt to send their children to college.

Education is an investment, but is college worth going into debt for? An education fund may help to cover some higher education costs. It could also be used for other education-related activities if you or your children decide not to attend college.

There can also be an education fund. If you have children, this could be where money is saved to help pay for their college. College may or may not be a significant investment. It will depend on how you view the modern education system, what a child’s degree is in, and other variables (such as getting work experience).

Education is a broad category. It could also include money saved to take a digital course that interests you or your children. It could be to pay for online homeschooling. It could be visiting a city or another country to learn more about the world and to gain valuable life experiences.

Education is a lifelong process. The money in the education fund can be devoted to self-learning and educating children. Plan by building an education fund to help improve continual learning.

Secure Single’s Algorithm recommends:

Summary

An emergency fund is vital to have. It provides some level of financial security. It could help to cover car issues that arise. Money saved for the intentional purpose of only being used for other emergencies can be separated into different accounts. Discover your ideal emergency fund as you begin your financial journey, but do not be afraid to add to it as your net worth grows.

Why not become a secure single?

How could an emergency fund help you to feel more financially secure?

👉 If you enjoy this post, consider sharing it with friends! Or feel free to click the ❤️ button so more people can find it on Substack! Or, do both! 🙏

Views expressed in this article are the author's opinions and do not necessarily reflect the views of Secure Single. It is intended for informational and educational purposes only. It is not investment, financial, or legal advice. Consult with a financial or legal professional before making an investment or legal decision. James Bollen is the author of Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate). It is now available in paperback and for the Kindle on Amazon.

| A guest post by

|

3 - 6 months of funds within a cash interest account. Other funds, if any, should be working for you with a risk you are able to tolerate.

Credit cards can work for urgent events aswell (no regular spending), however, a corresponding amount should be free to pay credit back asap.