Revealing The Hidden Connection Between Money, Wealth, And Well-Being

Money and wealth are the backbone to your overall well-being and happiness.

You've heard the saying that "money can't buy happiness." The truth is more nuanced.

While money and wealth won't fulfill you, financial insecurity can destroy your peace of mind.

Find the sweet spot by earning enough money and having a high enough net worth to eliminate financial stress so you can spend more time focusing on relationships, experiences, and personal growth.

However, the economic landscape in the United States makes this particular balancing act challenging. Housing costs have skyrocketed while wages remain stagnant. Combine wage stagnation with the constant pressure of rising living costs, inflation, and currency debasement. The result is that many people are stuck in a state of survival mode.

Discover the hidden connection between money, wealth, and well-being!

Problem: When Financial Instability Controls Your Life

Soomin Ryu and Lu Fan found in a study that:

"Growing evidence reveals that financial strains and worries play significant roles in mental health."

According to the University of Wyoming, Financial stress can cause:

Heart Disease/Attack

Gastrointestinal Problems

Weight Gain/Loss

Eating Disorders

Diabetes

Insomnia

Psoriasis

Cancer

High Blood Pressure

Substance Abuse

Financial instability isn't just discomfort. Financial anxiety is your body's reaction to perceived danger.

The danger is being unable to fully provide for yourself, save money to pay off debt, and invest to grow your wealth so you can retire.

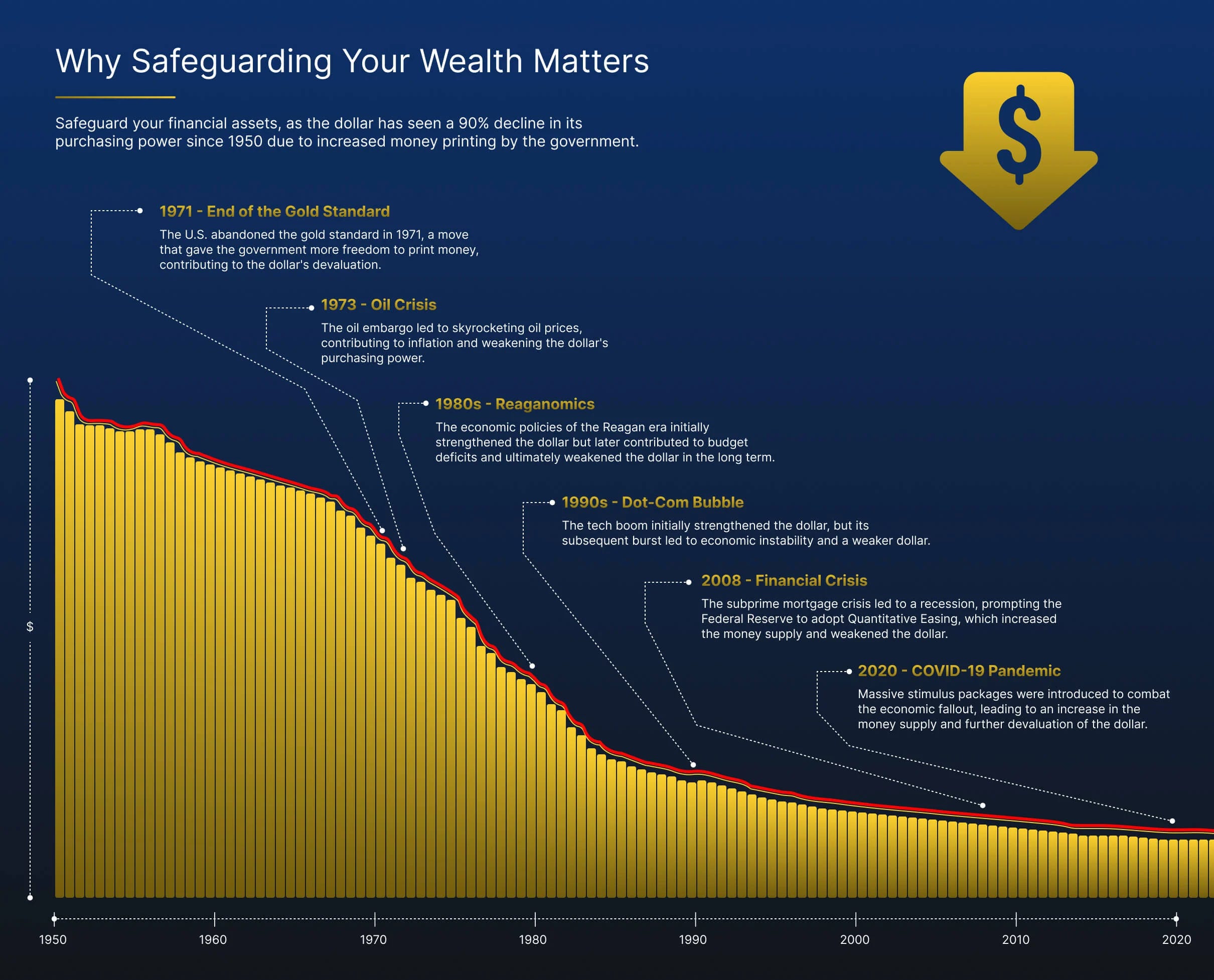

Debt-Based Economy

The debt-based economy and currency debasement increase financial pressures. The central bank's quantitative easing, the government deficit, and credit card debt all contribute to inflation.

Inflation and currency debasement lead to a cost-of-living crisis, making it difficult for you to survive financially, let alone thrive.

Median Home Price To Median Income

Redfin's housing market data from May 2025 shows that the current median home sale price in the United States is just under $450,000.

Boundless Estates notes that to afford a house in the United States at the current median price, you would need to earn an annual income of $114,000.

The majority of Americans don't earn a six-figure income, which means homeownership is only possible for those in the top income brackets.

Living Paycheck To Paycheck

According to Market Watch, 57% of Americans live paycheck to paycheck.

Living paycheck to paycheck is a consequence of a combination of problems, including the cost of living (necessities), rising inflation, wage stagnation, and not following a budget.

Debt

There are different types of debt. Common types of debt are credit cards, auto loans, and student debt.

Credit Card Debt

LendingTree writes:

"The national average card debt among cardholders with unpaid balances in Q1 2025 was $7,321, up 5.8% from $6,921 in Q1 2024. That includes debt from bank cards and retail credit cards."

Lending Tree describes in the same article that the typical credit card APR is 21%.

Auto Loans

LendingTree found that the price of used cars rose by 1.8%, and the average monthly payment for Americans is between $600 and $800.

Student Debt

According to The College Investor, the average student debt level by degree ranges from $19,270 for an Associate's Degree, $26,190 for a Bachelor's Degree, and $106,850 for a Graduate Degree.

Intelligent found that "only 46% of college grads surveyed say they currently work in their field of study," and that "48% of college graduates live paycheck to paycheck" all or most of the time.

A college degree does not mean that you'll get a good-paying job after graduation. You'll end up with more debt. That's why more millennials and Gen Z are questioning the value of a college education.

Consequences Of Debt Traps

You'll trap yourself in a reactive financial mode by being in debt without proper savings and depreciating assets. You'll constantly be putting out financial fires. You'll never build lasting wealth and appreciating assets.

Key Point: Chronic financial instability creates biological stress responses that undermine every aspect of well-being.

Solution: A Step-by-Step Wealth Building Framework

Phase 1: Establish Your Financial Foundation (Months 0-6)

The good news is that there are always solutions. Even if you have debt, you can pay it off and work to build wealth by following some simple financial strategies.

The Upgraded 50/30/20 Budget

The upgraded 50/30/20 budget is a variation of the traditional 50/30/20 budget. The traditional 50/30/20 budget recommends using 50% of your total income to needs, 30% to any wants, and your remaining 20% to paying off debt and saving for emergencies.

The new and improved 50/30/20 budget works as follows.

50% For Needs

50% of your monthly income still goes towards necessities.

Needs include your:

Rent or mortgage.

Utilities

Healthcare.

Insurance (auto, health, and renters).

Groceries.

Transportation.

30% For Debt, Savings, And Investing

30% goes toward paying off your debt, savings, and investing in your future. Prioritize aggressively paying off your debt first. If you have no debt, you have an extra 10% that you can save and invest every month.

20% For Fun

You can still have fun. Your remaining 20% is for doing activities that you enjoy. Just make sure not to go overboard.

While it's important to enjoy life, short-term pleasure is less important than long-term planning for your personal and financial future.

Pro Tip: Automate transfers so savings happen automatically before you see the money in your bank account.

Related

Phase 2: Build Your Wealth Engine (Months 6-24)

Focus on building your wealth engine over the next six to twenty-four months.

3-Bucket Emergency Fund

The three-bucket emergency fund is a strategy that helps you work to build your emergency fund. You want an emergency fund for when unexpected financial emergencies happen.

Bucket #1

Your first financial goal is building a starter emergency fund of $1,000. Your starter fund lays the foundation for freeing you from financial stress. Your starter fund helps you to cover any smaller unplanned financial emergencies.

Bucket #2

The second bucket is building a six-month financial buffer to help you last if you lose your job. You can find an emergency fund calculator online to determine how much you need in your six-month financial buffer.

Be sure to include the cost of your monthly necessities and the amount of time you'll need to survive until you find another job. It could take you longer than six months.

Bucket #3

The third bucket is to cover all your fixed expenses over a one-year period. You want this in case it takes you longer to find another job, you have a medical emergency, or unplanned life events happen.

It's always a good idea to continue to grow your emergency fund. Keep your emergency fund in a separate high-yielding savings or money market account. Your rainy day fund is separate from your basic savings account and earns a higher interest rate.

Key Point: Prioritize building an emergency fund so that you have money to fall back on for unplanned life emergencies.

Phase 3: Start Investing (12 -24 Months)

Your employer may offer you a matching 401(k). You should check with your employer and read your employee manual. If you work a part-time or gig job, you may not have a 401(k). But it's always good to check.

Roth IRA

Create a Roth IRA account with Fidelity, J.P. Morgan, or Charles Schwab. A Roth IRA gives you tax-free growth. You can invest $7,000 a year into a Roth IRA. You're free to invest in individual stocks, index funds, and bonds.

Index Funds

If you're unsure where to begin, start investing in index funds. Index funds allow you to invest across the stock market according to the type of index you choose. Low-cost index funds include indexes that track the S&P 500, VTI, and VXUS.

The great thing about index funds is that they're passive and still grow.

Key Point: Invest in the stock market through a 401(k), Roth IRA, and by buying index funds.

Phase 4: Optimize And Accelerate (Year 2+)

Once you've established your financial foundation, you want to optimize and accelerate your finances.

Increase Your Earnings Ceiling

Identify two to three high-paying skills that you can hone and improve in your field. Depending on your field, you may need to learn new skills and make a career change.

Dedicate five hours a week to upskilling. You want to focus on building high-paying skills. Having high-paying skills allows you to earn more money and makes it harder for you to be replaced. Continue to master a skillset and become a lifelong learner.

Once you've upskilled, you've several options. Be confident and negotiate a raise from your employer. You can pivot to a higher-paying field or role. You can begin freelancing or consulting. You can start your own online business.

Create Passive Income Streams

Passive income streams allow you to reclaim your time. Time is your most valuable asset. You can then use your time to spend with the people you love, travel, pursue your hobbies, and do what makes you most happy.

Dividend Paying Stocks

Invest in dividend-paying companies to earn passive income. Look for companies with a high payout ratio and a consistent history of paying out dividends to their shareholders.

Advertisements

Google AdSense pays you per 1,000 views on a website and YouTube. Ads run 24/7 while you sleep. As your website or YouTube Channel grows, you'll earn more income.

Digital Assets

Sell digital courses using Teachable, Thinkific, or Kartra. Sell digital and physical products on e-commerce sites like Gumroad, Etsy, and Amazon.

Key Point: Wealth building happens in various phases. Master the fundamentals before chasing more advanced strategies.

Why This Matters: Your Freedom Dividend

Financial security yields dividends that benefit both your financial well-being and overall well-being, extending far beyond your bank balance.

The Gift Of Time

Wealth allows you to stop trading your hours for time. When you're working forty to eight hours a week, you're unable to spend it doing what matters the most to you.

Money allows you to reclaim your time by enabling you to retire early. You can enjoy spending more time with your friends, family, and community. You can spend more time exercising and following a better diet to lose weight. You can spend more time on your hobbies. You can take work sabbaticals. You can work fewer hours each day.

Time is your most valuable asset. You now have time working for you, rather than against you. You decide how you want to use your time.

Stress-Free Relationships

Money fights disappear. You can be generous with loved ones who are struggling financially. You can help your friends, family, or relatives who need extra help so that they don't go into debt.

You can teach your children, friends, and family how to manage their finances better if they are interested in learning about money management and building wealth.

Opportunity Capital

When you have six to twenty-four months of living expenses, you have more options.

Career Risks

You can take more risks by taking longer to apply for jobs, as you have money to fall back on. You can work to transition to a new field. You can invest in learning new in-demand skills that will pay you more.

Start A business

You have capital available to start a business. You don't need to get a loan from a bank to start your business. Today, you can start an online business for under $1,000 or for free. It just depends on how formally you want to set it up. It's better to set it up formally as a business for tax and legal reasons.

Travel

You have more time to travel, explore your state, country, and the world. Traveling allows you to learn about how people live outside of your home country and culture. You can stay and talk to locals, find travel guides, and enjoy longer vacations without having to worry about missing work.

Compound Your Happiness

The psychological benefit of financial security grows over time.

Each year of financial stability makes your next year easier. You can save and invest more.

Financial freedom boosts your confidence. You have the freedom to live your life because you don't always have to work.

You can then spend your time on activities that bring you the most happiness.

Key Point: Real wealth isn't about making luxury purchases. Real wealth is about prioritizing your freedom, security, and well-being.

Related

Summary

Real wealth helps you stop worrying about being unable to pay for your credit card bill or medical expenses.

Financial security allows you to reclaim your time. You can spend it with the people and doing the activities that matter most to you.

Financial freedom lets you invest in your health, allowing you to live a longer life.

Financial well-being is about making informed financial choices so you can control your happiness. Lasting well-being comes from consistent small steps that compound into financial freedom.

Disclaimer: This content is for educational, entertainment, and informational purposes only. This is not business, financial, investment, or any advice. I write online about topics that interest me. I make mistakes just like everyone else. Always conduct your own research and consult a professional before making decisions regarding health, life, finances, investments, taxes, or legal matters.